Stocks and bonds are not at odds with each other

I'm seeing more and more observers commenting on the apparent disconnect between the stock and bond markets. Reader "Rob" recently linked to a

post by Thomas Kee at Smart Money that is typical. Kee argues that bond buyers these days are likely smarter than equity investors, because "they are educated and intelligent, and they make decisions for longer-term purposes.

" Whereas equity investors are more short-term focused ("fast money") and currently have been lulled into believing the recovery is real, when in fact it is "fabricated."

I think it's very difficult to defend the belief that one class of investors (bond buyers) see the world differently than another class (equity buyers), when both operate in the same capital market and both have access to the same information. To assert this, however, I need to show how it is that bond and equity investors today share similar beliefs about the economic fundamentals. If I'm right, then the "disconnect" is not really a disconnect, it's simply the result of how two very different asset classes react to the same information.

The chart above is a good illustration of the alleged "disconnect" between the stock and bond markets. Over the past three years, stock prices have been in a rising trend, while bond yields have been in a falling trend. That doesn't make sense, so the thinking goes, because falling bond yields are symptomatic of a market that is increasingly risk-averse, whereas rising equity prices are symptomatic of a market that is increasingly risk-loving. I think both interpretations are wrong.

As the first chart above shows, there is a decent correlation between the level of real yields and the strength of the economy. Real yields and real economic growth were both quite high in the late 1990s and early 2000s. The economy had been booming for several years, and the market expected this to continue. The real yield on TIPS had to compete with the very strong real yields on equities. This makes perfect sense. Now, over a decade later, real yields on TIPS are negative and the economy is in the midst of its weakest recovery ever, with a so-called "output gap" that could be

as much as 13%. As the second chart shows, consumer confidence is extremely low; although it has risen in recent years, it is still at levels that in the past have coincided with recessions. The first chart suggests that the level of real yields is consistent with market expectations of almost zero growth for the next several years.

As the chart above shows, the equity risk premium—defined here as the difference between the earnings yield on equities minus the yield on 10-yr Treasuries—is extremely high. Why would the market be indifferent between an almost 5% earnings yield on equities and a paltry 1.7% yield on 10-yr Treasuries? The only explanation that makes sense is that the market has almost no confidence that corporate profits will maintain their current levels; instead, the market fully expects

profits to decline significantly.

As the chart above shows, the earnings yield on equities tends to track inversely the real yield on TIPS. In other words, when real yields fall, as they have over the past decade, the earnings yield on equities has risen. The more gloomy the market becomes over the prospects for economic growth, the higher the equity yield that the market demands in compensation for what is expected to be a big decline in profits. The two lines have diverged of late, and perhaps that is significant, but such divergences have happened before.

As the chart above shows, it is very unusual for the earnings yield on equities to be higher than the yield on BAA corporate bonds. Would you pass us the opportunity to buy stocks with a higher earnings yield than available on corporate bonds if you thought the economy was going to be healthy? No, because that would mean giving up the opportunity for price appreciation. Investors today are willing to accept a lower yield on corporate bonds because bonds are higher in the capital structure and have first claim to earnings, which the market suspects may be in for trouble.

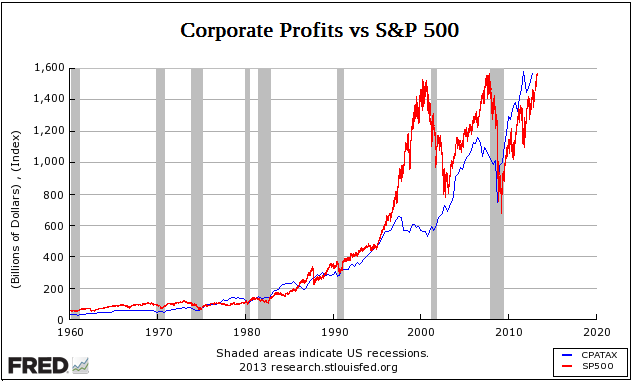

But what about the fact that stock prices are at all-time highs? Doesn't that conflict with the fact that Treasury yields are close to all-time lows? Not necessarily. As the chart above shows, in inflation-adjusted terms the S&P 500 is still almost 25% below its 2000 all-time high. From a long-term perspective, the chart suggests that current equity prices are about "average," having followed a 3% trend growth rate, which happens to be the average real growth rate of the U.S. economy. Moreover, corporate profits today are almost 200% above the levels of late 2000. By these metrics, stocks are not optimistically priced at all. Today's S&P 500 PE ratio is just above 15, which is below its long-term average of 16. Shouldn't PE ratios be much higher than average considering that risk-free discount rates are at all-time lows?

Bonds and stocks are both priced to pessimistic assumptions about the future health of the U.S. economy, no matter how you look at it. And as for the assertion that the recovery has been "fabricated," I refer the reader back to many of my posts which show abundant evidence that many sectors of the economy are posting solid, undeniable growth, beginning with

this recent post. This recovery may be the weakest ever, but it is no less real because of it.